Professional Analysis of How COVID-19 is Impacting the Synthetic Biology Market

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=889

- North America (US and Canada)

- Europe (Germany, France, UK, Spain, RoE, Denmark, Switzerland & Italy)

- Asia-Pacific (China, Japan, India, Australia and Rest of Asia Pacific)

- Rest of World (Latin America, Middle East & Africa)

Professional Analysis of How COVID-19 is Impacting Synthetic Biology Market

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=889

- North America (US and Canada)

- Europe (Germany, France, UK, Spain, RoE, Denmark, Switzerland & Italy)

- Asia-Pacific (China, Japan, India, Australia and Rest of Asia Pacific)

- Rest of World (Latin America, Middle East & Africa)

Autoinjectors Market | Newest Industry Data, Future Trends and Forecast 2023

Autoinjectors are used to self-administer drugs for the treatment of various diseases and conditions, such as rheumatoid arthritis, multiple sclerosis, diabetes, and anaphylaxis. Autoinjectors are easy to use, portable, and improve dosing accuracy, making them one of the most popular methods for the self-administration of drugs.

The global autoinjectors market is projected to reach USD 85.31 billion by 2023 from an estimated USD 28.91 billion in 2018, at a CAGR of 24.2% during the forecast period (2018-2023).

In terms of Therapy, the global autoinjectors market can be segmented into:

Rheumatoid Arthritis

Multiple Sclerosis

Diabetes

Anaphylaxis

Other Therapies (Cardiovascular Diseases, Migraines, Psoriasis, and Anemia)

By therapy, the rheumatoid arthritis segment is expected to account for the largest share of the market in 2018

On the basis of therapy, the autoinjectors market is segmented into rheumatoid arthritis, multiple sclerosis, diabetes, anaphylaxis, and other therapies such as migraines, cardiovascular diseases, psoriasis, and anemia. In 2018, the rheumatoid arthritis segment is expected to account for the largest share of the global market. The large share of this segment can be primarily attributed to the high prevalence of rheumatoid arthritis across the globe.

Get a sample PDF copy of the Report @: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=173991724

Autoinjectors are easy-to-handle and cost-effective medical devices that can be used by patients, caregivers, and even untrained personnel to deliver a dose of a particular drug. Autoinjectors are used by patients to manage autoimmune diseases and chronic diseases. They are used for a wide range of indications such as rheumatoid arthritis, multiple sclerosis, diabetes, and anaphylaxis.

The geographical regions mapped in the report are:

- North America

- Europe

- APAC

- Rest of the World

North America to dominate the market in 2018

In 2018, North America is expected to account for the largest share of the autoinjectors market, followed by Europe. Factors such as increasing geriatric population in Canada, increasing FDA approvals, rising prevalence of anaphylaxis in the US, and rising prevalence of autoimmune and chronic diseases in the US and Canada are contributing to the large share of North America.

Some key players mentioned in the research report are:

The key players in the global autoinjectors market are Abbvie (US), Amgen (US), Teva (Israel), Biogen (US), Eli Lilly (US), and Mylan (US). The other prominent players in the market are J&J (US), Novartis (Switzerland), Bayer (Germany), Merck (Germany), Biogen (US), Ypsomed (Switzerland), SHL Group (Taiwan) Becton, Dickinson and Company (US), Owen Mumford (UK), Novartis (Switzerland), and Haselmeier (Switzerland).

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=173991724

Potential Impact Of COVID-19 On Drug Screening Market | Leading Companies Analysis 2022

Factors such as growing drug & alcohol consumption, enforcement of stringent laws mandating drug and alcohol testing, and regulatory approvals and new product & service launches are driving the growth of the market.

What the Market Looks Like?

The drug screening market was valued at USD 4.86 Billion in 2016 and is expected to reach USD 8.63 Billion by 2022, growing at a CAGR of 10.2% during the forecast period. The base year considered for the study is 2016 and the forecast period is from 2017 to 2022. The market is dominated by North America, followed by Europe, Asia Pacific, and the Rest of the World (RoW).

The global market by sample type is segmented into urine, breath, oral fluid, hair, and other samples. The urine sample segment is estimated to account for the largest share in 2017, however, the oral fluid samples segment is expected to register the highest growth rate during the forecast period.

Get a sample PDF copy of the Report @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=162987773

What Drives the Market?

The growth of the global market for Drug Screening Market is primarily influenced by the following factors:

1 Growing Drug & Alcohol Consumption

2 Enforcement of Stringent Laws Mandating Drug and Alcohol Testing

3 Presence of Government Funding in Major Markets

4 Regulatory Approvals & Product Launches and Services

The study involved four major activities to estimate the current market size for particle therapy. Exhaustive secondary research was done to collect information on the market and its different subsegments. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research.

The drug screening market is highly competitive with the presence of several big and small players.

Prominent players offering products for drug screening include Alere (US), Thermo Fisher (US), Drägerwerk (Germany), OraSure (US), Alfa Scientific Designs (US), Lifeloc (US), MPD, Inc. (US), Premier Biotech (US), Shimadzu (Japan), Siemens Healthineers (US). On the other hand, LabCorp (US),etc

Read more about Drug Screening Market @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=162987773

Vaccine Adjuvants Market Analysis and Opportunities During COVID-19 Pandemic

The global vaccine adjuvants market consists of human and veterinary adjuvants that are used to improve the efficacy of vaccines. This market is driven by several factors such as increasing government funding for research, high prevalence of diseases, expanding biotechnology and biopharmaceutical industries, and growing focus on prevention of diseases.

- The global vaccine adjuvants market is expected to reach USD 769.4 Million by 2021 from USD 467.0 Million in 2016, at a CAGR of 10.5%.

What Drives the Market?

1. Increasing Use of Adjuvants in Vaccine

2. High Prevalence of Infectious and Zoonotic Diseases

3. Increase in Livestock and Instances of Diseases

4. Increasing Focus on Immunization Programs From Various Government Bodies

5. Technological Advancements in Aluminum Hydroxide-Based Adjuvants

The research applications segment is expected to account for the largest share of the market during the forecast period. The human vaccine adjuvants segment is expected to account for the largest share of the global market in 2016 and is expected to have a higher growth rate in the application category segment.

Get a sample PDF copy of the Report @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=152603894

The global market is broadly classified into product type, route of administration, disease type, applications, and application categories.

On the basis of product type, the vaccine adjuvants market is segmented into pathogen components, adjuvant emulsions, particulate adjuvants, combination adjuvants, and others. The particulate adjuvants segment is expected to account for the largest share of the global market in 2016.

On the basis of disease type, the vaccine adjuvants market is segmented into infectious diseases, cancer, and others. The infectious diseases segment is expected to account for the largest share of the global market in 2016. Factors such as high prevalence of infectious diseases, government & company initiatives, and high prevalence of cancer cases are expected to drive market growth in the coming years.

The geographical regions mapped in the report are:

1. North America

2. Europe

3. Asia-Pacific

4. Rest of the World (RoW)

The vaccine adjuvants market is dominated by North America, followed by Europe, Asia, and the Rest of the World (RoW). However, Asia is projected to grow at the highest CAGR during the forecast period. Growth in the North American segment is primarily driven by the increasing geriatric population and rising incidences of diseases in the North American countries

Some key players mentioned in the research report are:

Brenntag Biosector (Denmark), CSL Limited (Australia), SEPPIC (France), Agenus, Inc. (U.S.), Novavax, Inc. (U.S.), SPI Pharma, Inc. (U.S.), Invivogen (U.S.), Avanti Polar Lipids, Inc. (U.S.), MVP Laboratories, Inc. (U.S.), and OZ Biosciences (France).

Get Sample Report @https://www.marketsandmarkets.com/requestsampleNew.asp?id=152603894

1

1

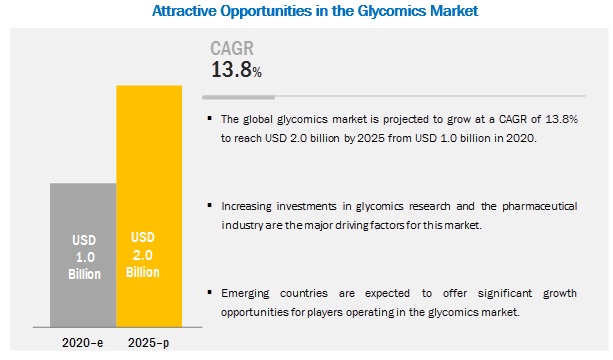

Glycomics Market COVID – 19 Updated Analysis By Top Key Players – Merck KGaA , Agilent Technologies, Shimadzu Corporation, Thermo Fisher Scientific

The growth of this market is majorly driven by the increasing research activities on glycomics, rising R&D investments in pharmaceutical and biotechnology companies, growth in the proteomics market. On the other hand, emerging countries such as India and China providing lucrative opportunities for players operating in this segment.

The global glycomics market is estimated to grow from USD 1.0 billion in 2020 to USD 2.0 billion by 2025, at a CAGR of 13.8%.

Glycomics / Glycobiology Market by Product (Enzymes (Glycosyltransferase, Glycosidase), Instruments (Mass Spectrometry, Chromatography), Carbohydrates, Reagents & Chemicals), Application (Disease Diagnostics), End-User (Academic) -Global Forecasts to 2025

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=132685525

The Global Glycomics / Glycobiology Market is Segmented on:

1. Product

2. Instruments

3. Application

4. End User

The demand for glycomics products for drug discovery & development is estimated to grow at a high rate during the forecast period

Based on application, the glycomics market is segmented into drug discovery & development, disease diagnostics, and other applications. Drug discovery & development is the largest and the fastest-growing application segment in the market, majorly due to the increasing R&D investments in pharmaceutical and biotechnology companies and the growing number of drug discovery research activities in academic research institutes.

Enzymes segment accounted for the largest share of the glycomics market, by product, in 2019

The market is categorized into five product segments, namely, enzymes, instruments, kits, carbohydrates, and reagents & chemicals. The enzymes segment is expected to dominate the market in 2020 and is projected to grow at the highest CAGR during the forecast period. The large share and high growth of this segment can be attributed to the consumable nature of enzymes and their wide applications in a variety of R&D and drug discovery procedures.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=132685525

Regional Analysis:

The global glycomics market is segmented into North America (US and Canada), Europe (Germany, the UK, France, Italy, Spain, and the Rest of Europe), Asia Pacific (Japan, China, India, Australia, and the Rest of Asia Pacific), and the Rest of the World (Latin America and the Middle East and Africa). In 2020, North America is expected to dominate the global market, followed by Europe.

Key Players:

Merck KGaA (Germany), Agilent Technologies (US), Thermo Fisher Scientific (US), New England Biolabs (US), Shimadzu Corporation (Japan), Takara Bio (Japan), S-BIO (subsidiary of Sumitomo Bakelite Co. Ltd., Japan), Waters Corporation (US), Asparia Glycomics S.L. (Spain), Bio-Techne (US), Bruker Corporation (US), Danaher Corporation (US), RayBiotech (US), Z Biotech (US), Chemily Glycoscience (US), Dextra Laboratories (UK), Lectenz Bio (US), and Ludger Ltd. (UK)

Professional Analysis of How COVID-19 is Impacting the Medical Device Reprocessing Market (2017-2022)

The medical device reprocessing includes cleaning, disinfection, inspection, sterilization, and repackaging of used medical devices for its reuse to diagnose and treat multiple patients. The reprocessing practices are regulated by various regional regulatory authorities. The changing regulatory scenario favoring medical device reprocessing in a number of countries, such as France and Japan, will open up new areas of opportunity for market players

The global medical device reprocessing market is projected to reach USD 1,754.0 Million by 2022 from USD 823.5 Million in 2017, at a CAGR of 16.3%.

Medical Device Reprocessing Market by Product (Reprocessed Device (Catheter, Endoscope, Laparoscopic Instruments, Biopsy, Pulse Oximeter), Service), Application (Cardiology, Gastroenterology, Arthroscopy, Orthopedic, Anesthesia) – Global Forecast to 2022

Medical Device Reprocessing Market, by Application

1. Cardiology

2. Gastroenterology, Urology, and Gynecology

3. Arthroscopy and Orthopedic Surgery

4. General Surgery and Anesthesia

Request Sample Report of Medical Device Reprocessing Market@ https://www.marketsandmarkets.com/requestsampleNew.asp?id=583

Drivers:

1. Low Prices of Reprocessed Medical Devices 2. Pressure to Reduce Volume of Regulated Medical Wast

The growth of this market is majorly driven by the increased utilization of the low priced reprocessed medical devices as compared to new devices, increased efforts towards reducing regulated medical waste (RMW), and rising number of surgical procedures associated with the growing prevalence of chronic diseases.

The report analyzes the market by product & service, type of medical device, application, and region. On the basis of product & service, the reprocessing support and services segment accounted for the largest share in 2016, owing to the increased adoption of third-party reprocessing services over in-house reprocessing services by hospitals, clinics, surgical centers, clinical pathologies, and other healthcare organizations

The geographical regions mapped in the report are: 1. North America 2. Europe 3. Asia-Pacific (APAC) 4.RoW

Geographically, the global medical device reprocessing market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. In 2016, North America dominated the market, and this is primarily attributed to its well-established healthcare industry, growing prevalence of chronic diseases, and increasing volume of surgical procedures.

Some key players mentioned in the research report are:

The major players in the global medical device reprocessing market are Stryker Corporation (U.S.), Johnson & Johnson (U.S.), Vanguard AG (Germany), Medline ReNewal (U.S.), Medtronic plc (Ireland), SteriPro Canada, Inc.(Canada), Pioneer Medical Devices AG (Germany), Vascular Solutions, Inc. (U.S.), HYGIA Health Services, Inc. (U.S.), ReNu Medical, Inc. (U.S.), SureTek Medical (U.S.), and Centurion Medical Products Corporation (U.S.).

Download PDF Brochure@ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=583

)

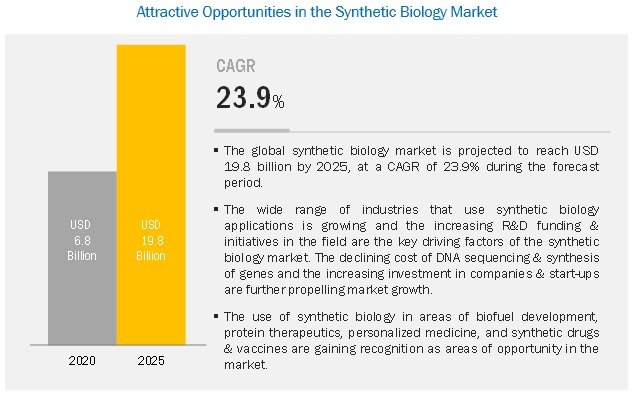

APAC is projected to be the fastest-growing High Performance Synthetic Biology Market

The synthetic biology market is projected to reach USD 19.8 billion by 2025 from USD 6.8 billion in 2020, at a CAGR of 23.9%.

The growth of this market is primarily attributed to factors such as the increasing demand for synthetic genes & synthetic cells, wide range of applications of synthetic biology, declining cost of DNA sequencing & synthesizing, increasing R&D funding & initiatives in synthetic biology, and increasing investments in the market.

Synthetic Biology Market by Tools (Oligonucleotides, Enzymes, Synthetic Cells), by Technology (Gene Synthesis, Bioinformatics), by Application (Tissue Regeneration, Biofuel, Renewable Energy, Food & Agriculture, Bioremediation) – Global Forecast to 2025

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=889

How much is the Synthetic Biology Market worth?

The synthetic biology market is projected to reach USD 19.8 billion by 2025 from USD 6.8 billion in 2020, at a CAGR of 23.9%. The growth of this market is primarily attributed to factors such as the increasing demand for synthetic genes & synthetic cells, wide range of applications of synthetic biology, declining cost of DNA sequencing & synthesizing, increasing R&D funding & initiatives in synthetic biology, and increasing investments in the market.

Download PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=889

Gene synthesis accounted for the largest share of the synthetic biology market in 2019 :

Based on technology, the market is segmented into gene synthesis, genome engineering, cloning, sequencing, site-directed mutagenesis, measurement & modeling, microfluidics, nanotechnology, and bioinformatics technologies. In 2019, the gene synthesis segment accounted for the largest share of the market.

The report claims to split the Regional Scope of the Focused synthetic biology Market into

- North America (US and Canada)

- Europe (Germany, France, UK, Spain, RoE, Denmark, Switzerland & Italy)

- Asia-Pacific (China, Japan, India, Australia and Rest of Asia Pacific)

- Rest of World (Latin America, Middle East & Africa)

The APAC market is expected to grow at the highest CAGR during the forecast period

The market in the Asia Pacific is expected to grow at the highest CAGR during the forecast period. Factors such as growth in the number of pharmaceutical & biopharmaceutical companies, the increasing number of healthcare & life science facilities, and increasing requirements for regulatory compliance in pharmaceutical and biopharmaceutical companies, growing number of international alliances, heavy funding for synthetic biology research, and strong government support are expected to drive the growth of these markets during the forecast period.

Which are the key players in the synthetic biology market and how intense is the competition?

The prominent players in the synthetic biology market are Thermo Fisher Scientific Inc. (US), Merck KGaA (Germany), Agilent Technologies, Inc. (US), Novozymes A/S (Denmark), Ginkgo Bioworks (US), Amyris, Inc. (US), Intrexon Corporation (US), GenScript Biotech Corporation (China), Twist Bioscience (US), Synthetic Genomics, Inc. (US), Codexis, Inc. (US), Synthego Corporation (US), Creative Enzymes (US), Eurofins Scientific (Luxembourg), Cyrus Biotechnology Inc. (US), ATUM (US), TeselaGen (US), Arzeda (US), Integrated DNA Technologies, Inc. (US), and New England Biolabs (US).

Infectious Disease Diagnostics Market – Analysis of Worldwide Industry Trends and Opportunities

Growth in this market is primarily driven by the increasing global prevalence of infectious diseases, shift in focus from centralized laboratories to decentralized point-of-care testing, and growth in funding for research on infectious disease diagnostics.

- The global infectious disease diagnostics market was valued at USD 13.93 Billion in 2016 and projected to reach USD 19.35 Billion in 2022, at a CAGR of 5.6%.

What Drives the Market?

1. Increasing global prevalence of infectious diseases

2. Shift in focus from centralized laboratories to decentralized point-of-care testing

3. Growth in funding for research on infectious disease diagnostics

Get a sample PDF copy of the Report @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=116764589

The global prevalence of infectious diseases such as influenza, HPV, hepatitis, HIV, and tuberculosis is considerably high in spite of significant improvements in sanitation practices and medicine. Many of the currently available diagnostic techniques are slow, involve complex procedures, and lack specific identification of causative agents.

On the basis of disease type, the infectious disease diagnostics (IDD) market is segmented into a wide range of diseases. Hospital acquired infections (HAI) segment to record the highest CAGR during the forecast period. Growth in HAI segment can be attributed to the rising burden of MRSA infections, the increasing number of new products launched in the market, and increasing adoption of technologically advanced HAI diagnostic tests such as BD MAX Cdiff assay, Xpert MRSA NxG, and ARIES C. difficile Assay that are based on PCR technology

The geographical regions mapped in the report are:

1. North America

2. Europe

3. Asia-Pacific

4. Rest of the World (RoW)

North America accounted for the largest share of the global infectious disease diagnostics market. The large share of this region is mainly attributed to the presence of a highly developed healthcare system, increasing prevalence of infectious diseases, the presence of a large number of leading national clinical laboratories, and easy accessibility to technologically advanced instruments in the region.

Some key players mentioned in the research report are:

Abbott Laboratories, Becton, Dickinson and Company, Biomérieux SA, Bio-Rad Laboratories, Danaher Corporation, Diasorin, Luminex, Meridian Bioscience, Quidel, Roche Diagnostics, Siemens AG, Thermo Fisher Scientific

Get Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=116764589

Biologics Safety Testing Market : Worldwide Industry Analysis and New Opportunities Explored

- The global biologics safety testing market is expected to reach USD 4.90 Billion by 2022 from USD 2.75 Billion in 2017, at a CAGR of 12.2% during forecast period.

2. Positive Trend of R&D Investments in Life Science

3. Increase in Number of Drug Launches

4. High Incidence and Large Economic Burden of Chronic Diseases

1. North America

2. Europe

3. Asia-Pacific

4. Rest of the World (RoW)

Particle Therapy Market to Receive Overwhelming Hike in Revenues by 2023

Particle Therapy Market by Type (Heavy Ion, Proton Therapy), Products (Cyclotron, Synchrotron, Synchrocyclotron), Services, System (Single-room, Multi-room), Cancer Type (Pediatric, Prostate, Breast), Application (Treatment, Research) - Forecast to 2023

The global particle therapy market is projected to reach USD 1,349 million by 2023 from USD 865 million in 2018, at a CAGR of 9.3%.The study involved four major activities to estimate the current market size for particle therapy. Exhaustive secondary research was done to collect information on the market and its different subsegments.

Request Sample Pages: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=12809137

1. Type

2. Products

3. Services, System

4. Cancer Type

5. Application

By product, the synchrotron segment is expected to grow at the highest rate during the forecast period

Synchrotrons are used to accelerate both protons and heavy ions such as carbon and hydrogen. The growth of the synchrotrons segment is attributed to factors such as the increasing number of research activities as well as the increasing investments in the development of synchrotron facilities.

By type, proton therapy is expected to be the largest contributor to the particle therapy market

The large share of the proton therapy segment can be attributed to factors such as the high degree of precision, shorter treatment time, and reduced side-effects associated with proton therapy as compared to conventional photon therapies using X-rays.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=12809137

Regional Analysis:

The Asia Pacific is one of the major revenue generating regions in the particle therapy market. China and Japan are the major countries responsible for the high growth of this regional market owing to factors such as the increasing per capita income, improving healthcare infrastructure, and supportive government activities in these emerging countries.

Key Players:

Ion Beam Applications SA (Belgium), Varian Medical Systems, Inc. (US), and Hitachi, Ltd. (Japan) are the major players operating in the particle therapy market. Other players in this market include Provision Healthcare (US), Mevion Medical Systems, Inc. (US), Sumitomo Heavy Industries, Ltd. (Japan), Optivus Proton Therapy, Inc. (US), ProTom International, Inc. (US), Advanced Oncotherapy Plc. (UK), and Danfysik A/S (Denmark)

Genotyping Assay Market 2018-2023 | Investment in Genotyping Process and Techniques to Boost Growth

The increasing incidence of genetic diseases and rising awareness of personalized medicine, growing importance of genotyping in drug development, and the increasing demand for bioinformatics solutions in data analysis are also expected to promote market growth in the coming years.

MarketsandMarkets forecasts the Genotyping Assay market to grow from USD 11.8 billion in 2018 to USD 31.9 billion by 2023, at a Compound Annual Growth Rate (CAGR) of 22.0% during the forecast period.

The study involved four major activities to estimate the current market size for particle therapy. Exhaustive secondary research was done to collect information on the market and its different subsegments. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size.

The major factors that are expected to be driving the Genotyping Assay market are technological advancements and the decreasing prices of DNA sequencing.

Browse 219 market data Tables and 53 Figures spread through 280 Pages

Download PDF Brochure Now:https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=249958595

Application of Genotyping assay market:

1. Pharmacogenomics

2. Diagnostic Research

3. Animal Genetics

4. bioinformatics

5. Agricultural Biotechnology

The objective of the report is to define, describe, and forecast the genotyping assay market size based on product & service, technology, application, end user, and region.

By technology, the sequencing segment to record the highest CAGR during the forecast period

The sequencing segment is expected to witness a faster growth rate in this market due to factors such as, the increasing application areas of DNA sequencing technologies, technological advancements, the availability of high-speed sequencing instruments, and the growing uptake of the hybrid approach of sequencing.

Regional Growth, Development and Demand Analysis:

North America is expected to hold the largest market size in the global genotyping market during the forecast period, followed by the European region. The increasing adoption of technologically advanced genotyping products, the high healthcare expenditure, presence of advanced healthcare infrastructure, highly developed healthcare systems in the US and Canada.

Request Sample Report of Genotyping Market: https://www.marketsandmarkets.com/requestsampleNew.asp?id=249958595

Key Players:

Illumina (US), Thermo Fisher Scientific (US), QIAGEN (Netherlands), Agilent Technologies (US), Danaher Corporation (US), Roche Diagnostics (Switzerland), GE Healthcare (US), Fluidigm Corporation (US), PerkinElmer (US), Eurofins Scientific (Luxembourg), Bio-Rad Laboratories (US), Pacific Biosciences of California (US), GENEWIZ (US), and Integrated DNA Technologies (US).

Illumina is the leading player in the genotyping market. The company led the sequencing market with its flagship NGS platforms—iSeq 100 system (launched in January 2018), NovaSeq 6000, HiSeq Series, MiSeq Series, NextSeq 500, and HiSeq X Ten & HiSeq X Five.

Varicose Vein Treatment Market to reflect impressive growth in Medical industry

2. To provide detailed information regarding major factors influencing the growth of the market in North America and Europe (drivers , restraints, 3. opportunities, and industry-specific challenges)

4. To analyze opportunities in the market for stakeholders and provide details of the competitive landscape for market leaders

4. To strategically profile the key players and comprehensively analyze their market shares

6. To estimate and forecast the market by mode and product in North America (US and Canada) and Europe (Germany, UK, France, Italy, Spain, and Rest of Europe)

Wireless Health Market | Advancements in Wireless Communication Technology

The global wireless health market is projected to reach USD 110.12 Billion by 2020 from USD 39.03 Billion in 2015, at a CAGR of 23.1% during the forecast period of 2015 to 2020. Growth in the overall market can largely be attributed to factors such as increasing advancements in wireless communication technologies, growing internet penetration, increasing utilization of connected devices in the management of chronic diseases, rising adoption of a patient-centric approach by healthcare providers, robust penetration of 3G and 4G networks in healthcare services, and mainstreaming of cloud computing.

Wireless Health Market by Technology (WPAN, WLAN/Wifi, WiMAX), Component (Hardware, Software, & Services), Application (Patient Specific and Provider/Payer Specific), & by End Users (Providers, & Payers) – Analysis & Global Forecast to 2020

Download PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=551

On the basis of components, the market is segmented into hardware, software, and services. The software segment accounts for the largest share of the global market in 2015. Increasing adoption of healthcare IT solutions and growing need for upgrading the existing software are the major driving factors for the growth of this market.

On the basis of technology, the market of wireless health is further segmented into WPAN, WLAN/WiFi, WiMAX, and WWAN. The WPAN technology market segment accounts for the largest share in the market in 2015. WPAN technologies are highly secure and affordable, making them one of the most widely adopted wireless health technologies. The WPAN technology segment is further segmented into Bluetooth, RFID, Ant+, ZIgbee, Z-wave, and UWB.

Request for Sample Pages @https://www.marketsandmarkets.com/requestsampleNew.asp?id=551

On the basis of end users, the market of wireless health is further segmented into providers, payers, and patients/individuals. The providers segment accounts for the major share of the global market in 2015.

Lack of skilled IT professionals and data security concerns are expected to restrain the growth of the market to a certain extent. In addition, lack of data management and interoperability issues pose as major challenges for the market. On the basis of region, this market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World (RoW).

Key Market Players

Allscripts Healthcare Solutions, Inc. (U.S.), AT &T, Inc. (U.S.), Cerner Corporation (U.S.), Omron Corporation (U.S.), Philips Healthcare (U.S.), Verizon Communications, Inc. (U.S.), Qualcomm, Inc. (U.S.), Aerohive Networks, Inc.(U.S.), Vocera Communications, Inc. (U.S.), and Alcatel-Lucent (U.S.) are some of the key players in the wireless health market worldwide.

Get More Information @https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=551

Which application segment dominates the digital therapeutics market?

The growth of the digital therapeutics market is primarily driven by factors such as government initiatives for preventive healthcare, technological advancements in mobile healthcare, a significant increase in venture capital investments, and the benefits of digital therapeutics, such as the ability to induce behavioral change (an important challenge in healthcare), user-friendliness, patient convenience, and improved drug compliance.

Digital Therapeutic (DTx) Market by Application (Prediabetes, Nutrition, Care, Diabetes, CVD, CNS, CRD, MSD, GI, Substance Abuse, Rehabilitation), Sales Channel (B2C, Patient, Caregiver, B2B, Providers, Payer, Employer, Pharma) – Global forecasts to 2025

The global digital therapeutics market is projected to reach USD 6.9 billion by 2025 from USD 2.1 billion in 2020, at a CAGR of 26.7% during the forecast period (2020–2025).

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=51646724

Global Digital Therapeutic (DTx) Market is Segmented on:

1. Application

2. Sales Channel

3. End user

Application

Based on the application, the digital therapeutics market is segmented into preventive and treatment/care-related applications. One of the key factors driving the growth of this segment is the rise in treatment and healthcare costs, especially due to chronic conditions.

Sales Channel

Based on the sales channel, the digital therapeutics market is segmented into business-to-customer (B2C) and business-to-business (B2B). In 2019, the B2B segment accounted for the largest market share; it is also expected to grow at the highest CAGR of the digital therapeutics market.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=51646724

Geographical Growth Analysis:

The global digital therapeutics market is segmented into North America, Europe, the Asia Pacific, and the RoW. In 2019, North America (US and Canada) held the largest share of the market, followed by Europe. The major factors supporting market growth include the increasing investments in digital therapeutics, the influx of new start-ups, improvements in the reimbursement structure for digital therapeutics, and government initiatives to support technological advancements

.

Key Market Players

Noom (US), Livongo Health (US), Omada Health (US), WellDoc (US), Pear Therapeutics (US), Proteus Digital Health (US), Propeller Health (US), Akili Interactive Labs (US), Better Therapeutics (US), Happify (US), Kaia Health (Germany), Mango Health (US), Click Therapeutics (US), Canary Health (US), Wellthy Therapeutics (India), Cognoa (US), Ayogo Health (Canada), Mindstrong Health (US), 2Morrow (US), and Ginger (US).

Cardiology Information System (CIS) Market Analysis as per the Latest COVID-19 Impact

Growth in this market is mainly driven by the increasing incidence and prevalence of cardiovascular disease, government initiatives in China, and the increasing number of hospitals.

- The China cardiology information system market is projected to reach $54 million by 2024 from $35 million in 2019, at a CAGR of 8.9% during the forecast period.

The software segment accounted for the largest share of the China cardiology information system market in 2018

By component, the market is segmented into software, services, and hardware. The software segment accounted for the largest market share in 2018. The large share of this segment can be attributed to the growing need to integrate CVIS with C-PACS, EMRs, and other cardiology modules.

Download PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=264168583

1.China Cardiology Information System Market, by System

> Integrated Systems

> Standalone Systems

2. China Cardiology Information System Market, by Component

>Software

>Services

>Hardware

3. China Cardiology Information System Market, by End User

>L3A Hospitals

>L3B and L2 Hospitals

The integrated systems segment is expected to grow at the highest CAGR during the forecast period

Based on system, the market is segmented into integrated and standalone systems. The integrated systems segment is projected to witness the highest growth during the forecast period. The increasing adoption of integrated systems by healthcare providers is the major factor supporting the growth of this segment.

Request for Sample Pages @https://www.marketsandmarkets.com/requestsampleNew.asp?id=264168583

L3A hospitals accounted for the largest share of the China cardiology information system market in 2018

Based on end user, the market is segmented into L3A hospitals and L3B & L2 Hospitals. The L3A hospitals segment accounted for the largest share of the market in 2018. The increasing number of L3A hospitals in China and growing disease prevalence are responsible for the large share of this market segment.

Key Market Players :

Key players in the China cardiology information system market are Philips Healthcare (Netherlands), CREALIFE Medical Technology (China), Central Data Network (Australia), Infinitt Healthcare (South Korea) and Esaote (Italy).

In 2018, CREALIFE Medical Technology held the leading position in the market. The company has good relations with government bodies, distributors, and hospitals in the market, which is its key strength. Philips Healthcare held the second position in the market in 2018.

Market Analysis as per the Latest COVID-19 Impact)